Coordinate Descent for Logistic Regression

A walk-through of two coordinate descent variants on cross-entropy loss for a binary UCI wine task, compared against scikit-learn's logistic regression baseline. Coordinate descent is a fundamental optimization tool in machine learning because it scales to high-dimensional problems, lets us update one parameter at a time, and underpins many modern large-scale training routines.

Introduction

This post showcases two different approaches to implementing coordinate descent on a model defined with cross-entropy loss. Coordinate descent can struggle with non-smooth multivariate functions, as the algorithm may get stuck at non-stationary points where level curves are not smooth. However, it has gained significant interest for large-scale problems, where it has proven competitive with other algorithms for training support vector machines and performing non-negative matrix factorization.

In this experiment I implement coordinate descent using the following approaches:

- Randomly optimize along a random coordinate

- Optimize along coordinate with the largest gradient in magnitude

To benchmark the solutions I implemented a standard logistic regression model without focusing on validation and was just used to obtain scikit-learn's implementation of gradient descent and final loss. The model is trained with the wine.data dataset provided by UCI machine learning repository.

Procedure

I use the cross-entropy loss \(L(w)\) in the coordinate descent method. Let \(\hat{y}\) be the probability of having label 1, and let \(y\) be the actual label. Then the cross-entropy loss and gradient is defined below:

\[ L(w) = -\frac{1}{n}\sum_{i=1}^{n} y_{i} \log \hat{y}_{i} + (1 - y_{i}) \log(1 - \hat{y}_{i}) \]

And thus the gradients with respect to each weight \(w_{j}\) is given by:

\[ \frac{\partial L(w)}{\partial w_{j}} = \sum_{i=1}^{n}(\hat{y}_{i} - y_{i})x_{j} \]

The loss function \(L(\bullet)\) should be differentiable and preferably convex. The procedure of the coordinate descent method is outlined below:

- Initialize weights to zero

- Get predictions from sigmoid function

- Calculate loss and gradients

- Find coordinate \(i\) with the largest gradient in absolute value (best coordinate descent) or randomly choose weight (random coordinate descent)

- Update weight \(i\) via: \(w_{i} = w_{i} - \eta \frac{\partial L(w)}{\partial w_{i}}\)

- Repeat steps until convergence

Data Preparation

import numpy as np

from tqdm import tqdm

from random import randint

import matplotlib.pyplot as plt

from sklearn.metrics import log_loss

from sklearn.metrics import accuracy_score

from sklearn.linear_model import LogisticRegression

data = np.loadtxt('./data/wine.data', delimiter=',')

X, y = data[:, 1:], data[:, 0]

# transform problem into binary classification task

idxs = [i for i in range(len(y)) if y[i] == 1 or y[i] == 2]

X, y = X[idxs], y[idxs]

# normalize data

X = (X - X.mean(axis=0))/(X.max(axis=0) - X.min(axis=0))

X = np.hstack((X,np.ones(len(X)).reshape(len(X),1)))

# transform target variable

y = np.array(list(map(lambda x: 0 if x == 1 else 1, y)))

Now that the data is prepared, we can use scikit-learn's implementation as our benchmark:

# scikit learn implementation (our benchmark)

reg = LogisticRegression(solver='sag', C=100000, max_iter=10000).fit(X,y)

L_star = log_loss(y,reg.predict_proba(X))

print("Loss L* = {:<16f}".format(log_loss(y,reg.predict_proba(X))))

Loss \(L^{*} = 0.000393\). We can now benchmark our coordinate descent implementations against this baseline \(L^{*} \approx 0.0004\). First let's define a few helper functions:

def sigmoid(x):

return 1 / (1 + np.exp(-x))

def cross_entropy_loss(y,y_pred):

loss = -(1/len(y))*np.sum(y*np.log(y_pred) + (1 - y)*np.log(1 - y_pred))

return loss

def cross_entropy_grad(y,y_pred,x):

return list(np.dot((y_pred - y),X)[0])

Best Index

For each iteration, only update weight \(w_{j}\) such that \(|\frac{\partial L(w)}{\partial w_{j}}|\) is the largest for all \(j\).

# initial weights

w = np.zeros(14).reshape(14,1)

w_rand = w

eta = 0.01

loss = []

loss_rand = []

num_iter = 1005000 # just take a bunch of iterations

for t in tqdm(range(num_iter)):

# predict step

y_pred = sigmoid(np.dot(w.T,X.T))

grad = cross_entropy_grad(y,y_pred,X)

largest = np.argmax(np.abs(grad)) # idx with largest magnitude

loss.append(cross_entropy_loss(y,y_pred))

# update that coordinate with largest gradient in magnitude

w[largest] = w[largest] - eta*grad[largest]

y_pred = sigmoid(np.dot(w.T,X.T))

y_pred = np.array(list(map(lambda x: 1 if x >= 0.5 else 0, y_pred.flatten())))

print("Accuracy for best coordinate descent {0}".format(accuracy_score(y, y_pred)))

print("Loss L = {0}".format(loss[-1]))

Accuracy for best coordinate descent 1.0

Loss = 0.0004698390523920375

Random Index

For each iteration, update weight \(w_{j}\) for \(j \in 0 \dots 13\) (e.g., randomly choose a coordinate to minimize on).

# initial weights

w = np.zeros(14).reshape(14,1)

w_rand = w

eta = 0.01

loss_rand = []

num_iter = 1005000

for t in tqdm(range(num_iter)):

# predict step

y_pred = sigmoid(np.dot(w.T,X.T))

loss_rand.append(cross_entropy_loss(y,y_pred))

grad = cross_entropy_grad(y,y_pred,X)

random = randint(0,13)

# update random coordinate

w_rand[random] = w_rand[random] - eta*grad[random]

y_pred = sigmoid(np.dot(w_rand.T,X.T))

y_pred = np.array(list(map(lambda x: 1 if x >= 0.5 else 0, y_pred.flatten())))

print("Accuracy for random coordinate descent {0}".format(accuracy_score(y, y_pred)))

Accuracy for random coordinate descent 1.0

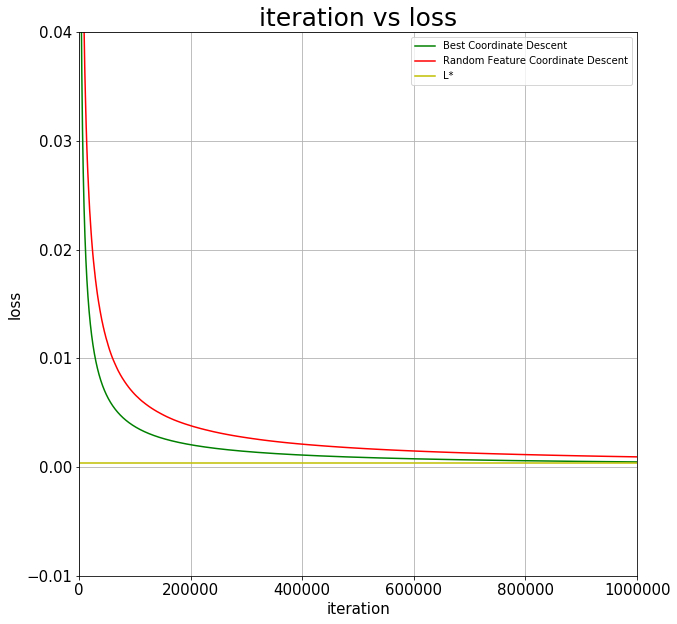

plt.figure(figsize=(10,10))

plt.plot(loss, 'g-', label='Best Coordinate Descent')

plt.plot(loss_rand, 'r-', label='Random Feature Coordinate Descent')

plt.axhline(y=L_star, color='y', label='L*')

plt.title('iteration vs loss', fontsize=25)

plt.xlabel('iteration', fontsize=15)

plt.xlim(0,1000000)

plt.ylim((-0.01,0.04))

plt.ylabel('loss', fontsize=15)

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.grid()

plt.legend()

Experimental Results

In this experiment I began by running an unregularized standard logistic regression solver from scikit-learn. The final cross-entropy of the logistic regression model is \(L^{*} \approx 0.0004\).

In my results, after 1.5 million updates, the coordinate descent method yields a loss \(L = 0.00047\), showing convergence to \(L^{*}\). It is important to note that both implementations of coordinate descent (random feature selection and best feature selection) converge to the loss \(L^{*}\), but at different rates.

We conclude that coordinate descent is more optimally implemented if the coordinate chosen has the largest gradient in magnitude. A clear advantage can be seen above from randomly choosing coordinates to update on.